Strait of Hormuz: World’s Most Critical Energy Chokepoint

A detailed strategic analysis of why the Strait of Hormuz, a narrow 33-kilometre waterway

between Iran and Oman, controls the flow of approximately one fifth of all oil consumed worldwide, and what a disruption would mean for global energy markets.

Author: Maria Hemmati Published: 28 April 2026

Data sourced from: EIA, IEA, Vortexa, Visual Capitalist, CNBC, Engineering News-Record (Q1 2025–2026)

20 mb/d

34%

~20%

~14 mb/d

Contents:

01 Overview & Geography · 02 Transit Volumes · 03 Exporters · 04 Asian Demand · 05 Bypass Options ·

06 Risk & Conclusion

Strategic Significance of the Strait of Hormuz

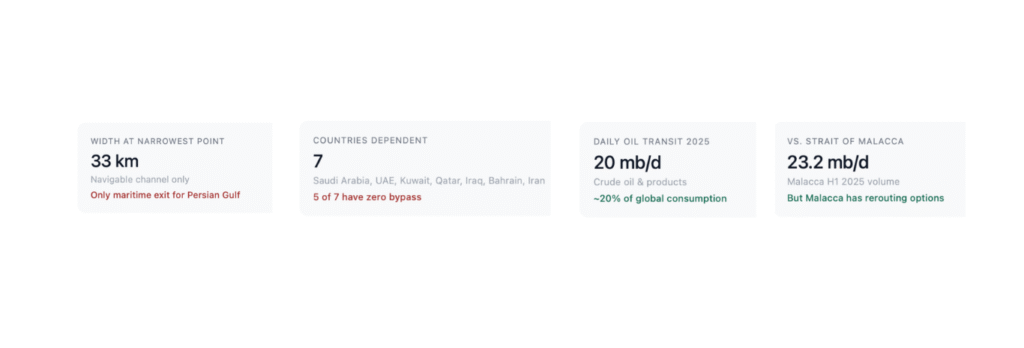

The Strait of Hormuz is a narrow waterway separating Iran to the north from the Omani enclave of Musandam to the south. At its narrowest navigable point, it is just 33 kilometres wide, yet this single passage is the only maritime exit route for all oil and gas produced across the entire Persian Gulf region.

Core finding: The Strait of Hormuz is categorically different from every other energy chokepoint in the world. It is the only door through which the Persian Gulf’s oil and gas can reach global markets by sea. Unlike the Strait of Malacca,where ships can detour through Indonesia’s Lombok or Sunda Straits at extra cost, there is no equivalent alternative for the Gulf. Iraq, Kuwait, Qatar, Bahrain, and Iran have no pipeline bypass infrastructure at all, meaning they are physically unable to redirect their exports even

if the Strait were closed for months.

Why is Hormuz uniquely irreplaceable?

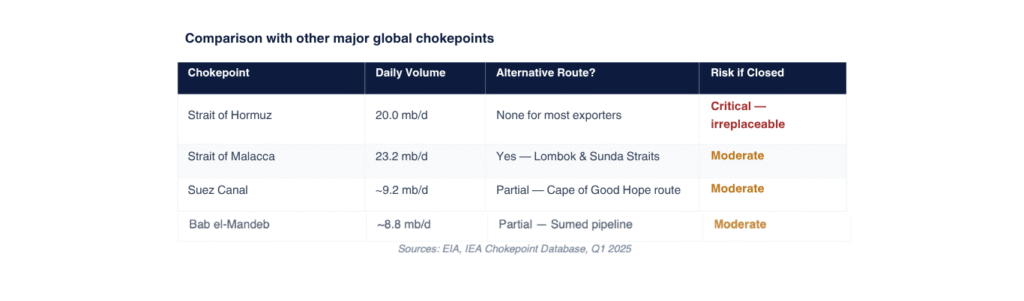

Most major energy chokepoints have workarounds. The Strait of Malacca, which carries even more daily volume than Hormuz, has viable alternative shipping lanes through Indonesian archipelago. The Suez Canal can be bypassed by sailing around the Cape of Good Hope at significant extra time and cost. The Strait of Hormuz has none of these options.

The reason is geography. The Persian Gulf is a semi-enclosed sea with only one opening: the Strait of Hormuz. All major oil-producing nations in the Gulf Saudi Arabia, Iraq, Iran, Kuwait, the UAE, Qatar, and Bahrain must pass through this single narrow point to reach the Indian Ocean and onward to global markets.

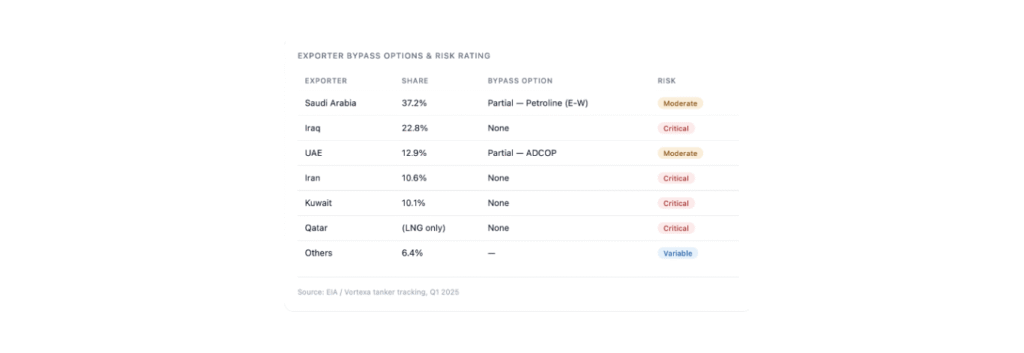

Saudi Arabia and the UAE have built partial bypass pipelines (the East-West Petroline and the ADCOP pipeline respectively), but these can handle only a small fraction of their normal export volumes. The other five major producers Iraq, Iran, Kuwait, Qatar, and Bahrain have no bypass infrastructure whatsoever.

The Extraordinary Scale of What Passes Through

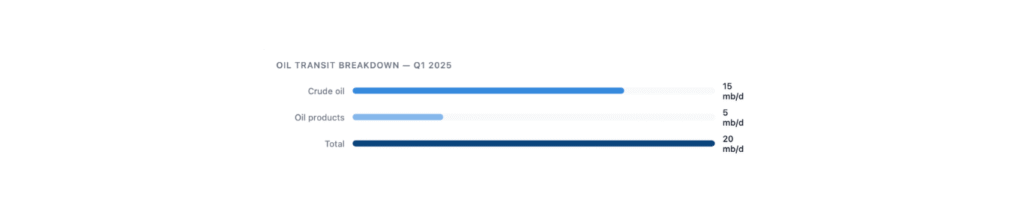

The volumes of oil and gas moving through this 33-kilometre bottleneck are staggering. In 2025, an average of 20 million barrels per day of crude oil and refined oil products passed through the Strait enough to fill roughly 1,000 large tankers every single day. This represents approximately 27% of all oil traded by sea anywhere in the world.

Oil transit breakdown . what exactly passes through

Of the 20 mb/d total, approximately 15 mb/d is crude oil, the unrefined petroleum that gets shipped to Asian refineries to be processed into fuel, plastics, and other products. The remaining 5 mb/d consists of refined products such as gasoline, diesel, and jet fuel. Together, these flows represent about one fifth of all oil consumed globally on any given day.

The LNG dimension often overlooked, equally critical

Beyond oil, the Strait is also critical for global liquefied natural gas (LNG) trade. LNG is natural gas that has been cooled to liquid form so it can be loaded onto specialised ships and transported around the world. Qatar is the world’s largest LNG exporter, and approximately 93% of its LNG shipments must pass through the Strait of Hormuz. The UAE routes about 96% of its LNG through the Strait. Together, Qatar and the UAE account for roughly 20% of all LNG traded globally.

If the Strait were closed, global LNG supply would fall by more than 300 million cubic metres per day that is more than double the total volume that used to flow through the Nord Stream pipeline from Russia to Europe in 2021. LNG processing facilities in other exporting countries (Australia, the USA, and others) are already operating at or near their maximum capacity, meaning there is no spare capacity available to quickly replace what would be lost.

Who Exports Oil Through the Strait and Who Has No Alternative

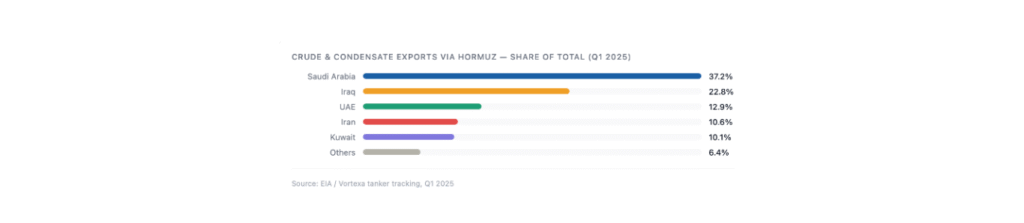

The oil and gas transiting the Strait comes from a concentrated group of Gulf producers. Just five countries Saudi Arabia, Iraq, the UAE, Iran, and Kuwait account for 93.6% of all crude oil and condensate flowing through. Understanding which of these nations has any bypass option, and which are completely locked in, is essential to understanding the true scale of the risk.

Strategic finding: For Iraq the second-largest contributor at 22.8% of all Hormuz crude flows the Strait is literally the only door through which its oil revenues can exit the country. Iraq has no pipeline bypass, no alternative port on a different sea. The same is true for Iran, Kuwait, Qatar, and Bahrain. Saudi Arabia and the UAE have partial pipeline alternatives, but these cover only a fraction of their normal export volumes leaving the vast majority still dependent on the Strait.

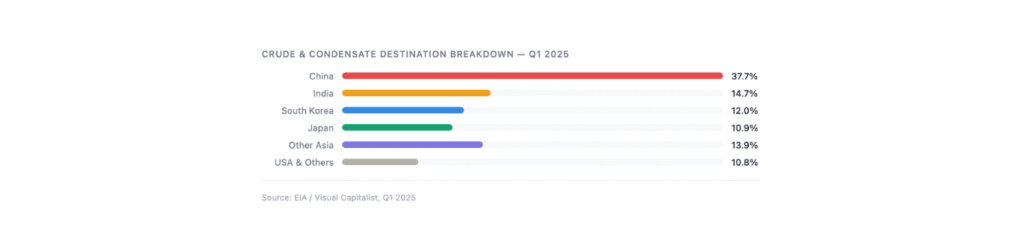

Asia Is the Destination And Has No Alternative Supplier

The oil and gas flowing through the Strait is overwhelmingly destined for Asia. Asian countries collectively receive 89.2% of all the crude oil and condensate that transits the waterway. This means that any disruption to the Strait would be felt most severely not in Europe or the Americas, but in the world’s fastest-growing economies China, India, South Korea, Japan, and others across the region.

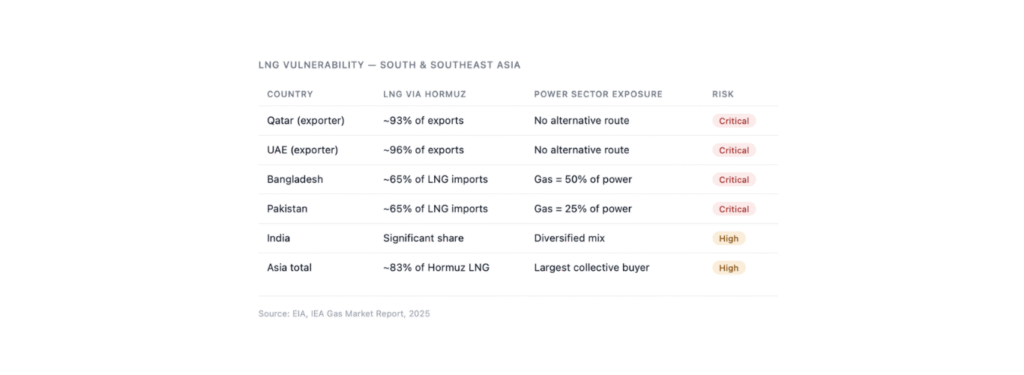

Key finding: China and India together received 44% of all crude oil flowing through the Strait in 2025. For both countries, switching away from Gulf oil is not possible in the short term, their refineries are physically designed to process Gulf crude, their long-term supply contracts are with Gulf producers, and their import port infrastructure is built around Gulf tanker deliveries. Bangladesh and Pakistan are even more exposed on the gas side: both countries imported approximately 65% of their total LNG through the Strait, and gas powers half of Bangladesh’s electricity grid.

LNG vulnerability in South & Southeast Asia

Beyond crude oil, the LNG exposure of South and Southeast Asian nations represents an acute vulnerability. Natural gas is the backbone of power generation in Bangladesh and Pakistan gas-fired power stations account for 50% of Bangladesh’s electricity and 25% of Pakistan’s. If LNG shipments were cut off by a Strait closure, both countries would face immediate electricity shortages, with cascading effects on industry, hospitals, water treatment, and daily life.

Why the Alternatives Fall Dramatically Short

A natural question is: could the oil and gas that normally flows through Hormuz be rerouted through pipelines or alternative shipping lanes if the Strait were closed? The answer is no not even close. While some pipeline capacity exists, it covers only a small fraction of what the Strait handles daily, leaving a massive unbridgeable gap with no practical solution.

Critical finding: Even if every available bypass pipeline were running at full capacity simultaneously, the combined throughput would be only 3.5 to 5.5 million barrels per day covering just 25–27% of the Strait’s normal daily flow. The remaining approximately 14 mb/d has no alternative route under any scenario. For LNG specifically, the situation is even more stark: there is simply no pipeline in existence capable of moving Qatari or UAE gas to global markets if the Strait closes.

The two bypass pipelines that exist and their limitations

There are only two meaningful pipeline bypasses for Persian Gulf oil exports:

1. Saudi Arabia’s East-West Petroline: This pipeline runs from Saudi Arabia’s Eastern Province oil fields westward across the Arabian Peninsula to the Red Sea port of Yanbu. It was designed to carry up to 5 mb/d, but the actual spare available capacity is significantly less closer to 3 mb/d. Even at maximum, it can handle only a fraction of Saudi Arabia’s normal exports, let alone the wider Gulf total.

2. UAE’s ADCOP Pipeline: This pipeline connects Abu Dhabi’s oil fields to Fujairah on the Gulf of Oman coast, effectively bypassing the Strait entirely. However, its capacity is only about 0.7 mb/d a relatively small contribution compared to the 20 mb/d that normally flows through the Strait.

Why LNG is even more exposed than oil

Unlike crude oil, which can theoretically be rerouted through pipelines or alternative tanker routes, LNG has almost no flexibility. There is no pipeline from Qatar to any alternative export terminal. If the Strait closes, Qatar’s LNG simply cannot reach the market, it would be stranded.

A Strait closure would remove over 300 million cubic metres per day from global LNG supply. To put this in perspective: this is more than double the volume that flowed through the Nord Stream pipeline from Russia to Europe in 2021 the same pipeline whose disruption caused Europe’s energy crisis. LNG liquefaction facilities in Australia, the USA, and other exporting countries are already operating at or near their maximum rated capacity, meaning there is no reserve capacity available to make up the difference, even in the medium term.

The World’s Most Irreplaceable Energy Chokepoint

Having established the scale of what transits the Strait, who it comes from, where it goes, and why it cannot be replaced, we can now assess the full risk picture. The Strait of Hormuz is not simply one geopolitical risk among many, it is the foundational risk that sits beneath all others in global energy markets.

Conclusion: In any period of escalating tension in the Middle East, the Strait of Hormuz occupies a unique position. A closure cannot be rerouted, replaced, or absorbed in the short term. The ~14 mb/d irreplaceable gap would trigger immediate and sustained oil price spikes, supply rationing across Asian economies, and simultaneous energy security crises in Bangladesh, Pakistan, South Korea, Japan, and India. The Strait of Malacca carries more daily volume, but it has alternatives. The Strait of Hormuz does not. That distinction is everything.

How a closure scenario would unfold impact by duration

The consequences of a Strait disruption scale dramatically with how long it lasts. Even a brief partial disruption causes immediate market panic and price spikes. A prolonged closure would represent one of the most severe supply shocks in the history of global energy markets.

Why Hormuz sits in a category of its own

The Strait of Hormuz stands apart from every other energy chokepoint because of the combination of three factors that no other passage shares simultaneously: the sheer volume of irreplaceable flows, the complete absence of adequate bypass alternatives, and the concentration of the world’s largest proven oil reserves and spare production capacity behind it.

Gulf OPEC+ nations Saudi Arabia, Iraq, the UAE, Kuwait, and Iran collectively hold the majority of the world’s recoverable petroleum reserves and the overwhelming majority of OPEC’s spare production capacity. This spare capacity is what the world relies on to manage oil price shocks and supply disruptions elsewhere. If the Strait closes, not only does this spare capacity become inaccessible, it is the very source of the disruption that the world would need to manage.

This is why, in any period of geopolitical escalation in the Middle East, the Strait of Hormuz is not simply one risk among many. It is the risk that all other risks are measured against.

© 2026 Maria Hemmati · Energy Market Intelligence · Published 28 April 2026 · All figures Q1 2025 unless otherwise noted · Sources: EIA, IEA, Vortexa, Visual Capitalist, CNBC, Engineering News-Record, Fitch Ratings, World Bank

Maria Hemmati

Energy Market Business Developer

")